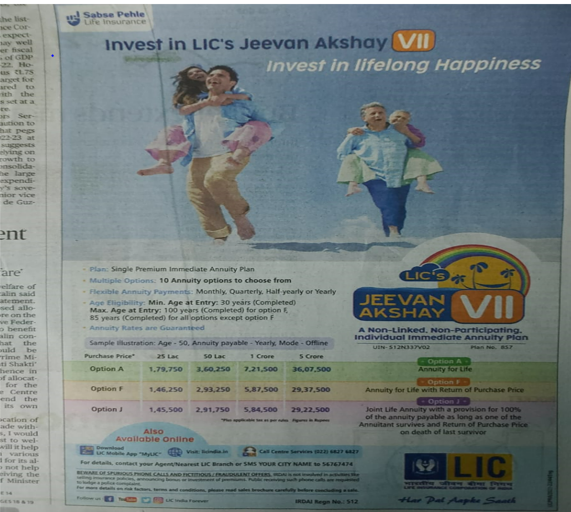

Jeevan Akshay VII (Plan 857) is an immediate annuity (Pension Plan) from LIC of India. Jeevan Akshay is a Non-Linked, Non-Participating, Individual Immediate Annuity Plan.

Let’s us be clear about what is annuity?

In simple term Annuity is regular income. Here we are looking at annuity as a pension plan.

Immediate annuity is investing lump sum on a product and you receive annuity from next month or next year.

Deferred Annuity is where your annuity starts after a certain period. You will invest up to your retirement age i.e. up to 60 years of age. After 60 years of age, your pension will start.

Though there are more than 10 options available under LIC Jeevan Akshay VII Pension Plan, the preferred annuity options for typical Indian families are A, F and J.

Plan features and benefits:

Option A: Immediate Annuity for Life. The annuity payments shall be made from the next year onwards (in arrears) for as long as the Annuitant is alive, as per the chosen mode of annuity payment. On death of Annuitant, nothing shall be payable and the annuity payment shall cease immediately.

Option F: Immediate Annuity for Life With Return of Purchase Price. The annuity payments shall be made from the next year onwards for as long as the Annuitant is alive, as per the chosen mode of annuity payment. On death of the annuitant, the annuity payment shall cease immediately and Purchase Price shall be payable to nominee.

Option J: Joint Life Immediate Annuity for Life . 100% of the annuity amount shall be paid in from next year onwards for as long as the Primary Annuitant and/or Secondary Annuitant is alive, as per the chosen mode of annuity payment. On death of the last survivor, the annuity payments will cease immediately and Purchase Price shall be payable to the nominee.

Annuity option once chosen cannot be altered

To Know more about LIC’s Jeevan Akshay plan visit: Life Insurance Corporation of India – LIC’s Jeevan Akshay – VII (Plan No. 857, UIN : 512N337V01) (licindia.in)

Returns Calculation:

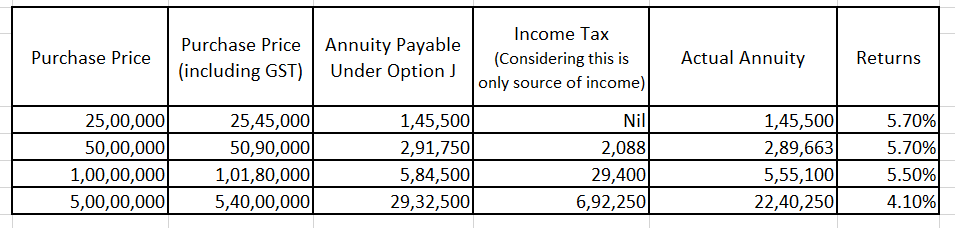

In LIC’s Jeevan Akshay plan, GST at the rate of 1.8% is applicable on the purchase price. We have added this to the calculations.

Only in Joint Life Immediate Annuity for Life(option J) 100% of the annuity amount shall be paid in from next year onwards for as long as the Primary Annuitant and/or Secondary Annuitant is alive. On the passing away of both the annuitants, the purchase price will be paid to the surviving nominee. This will be the most preferred option for any Indian Family. So the benefit illustation for this plan only is used for the calculations.

As it is a pension plan, the money you receive is taxable income as per your income tax slab. Considering that this is the only source of income, taxation has been calculated and actual annuity is derived in the below table. The tax rate could he higher in case there is any other source of income for the retiree.

Visit for taxation: Salaried Individuals for AY 2021-22 | Income Tax Department

Should you buy this pension plan? Definitely No.

If your annuity is the only source of income and considering taxation then the returns are much lower i.e., 4.1% to 5.7% only.

Team Financial Wellness suggests conservative hybrid mutual funds which are available in market with better returns. We can choose systematic withdrawal plan from these funds for the annuity.

Summary:

Team Financial Wellness recommends not to choose LIC Jeevan Akshay VII Pension Plan as:

- Returns generated is very low.

- The Annuity option once chosen is locked forever.

- Conservative hybrid mutual fund plan with systematic withdrawal plan gives much better returns.

©Copyright of Karthikeyan Jawahar; 2021 and beyond. All Rights Reserved. Any modification or use for commercial purpose without prior written consent by Karthikeyan Jawahar is prohibited. This article is for knowledge sharing purpose and should not be deemed as an implementation plan. Contact Team Financial Wellness for a customized plan implementable for you.

Leave a Reply